The ETH futures premium turned bearish and the network's TVL dropped 22% from its peak, but how is this impacting pro traders’ sentiment?

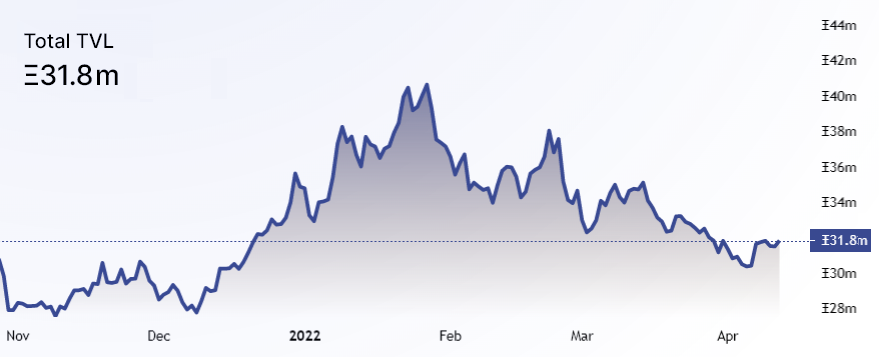

Ether (ETH) lost the critical $3,000 psychological support level on April 11 after a 16% weekly negative performance. Bulls were definitively caught by surprise as $104 million in leveraged long futures got liquidated on April 11. Ether's downturn also followed a decline in the total value locked (TVL) in Ethereum smart contracts.

The metric peaked at 40.6 million Ether on Jan. 27, and has since dropped by 22%. This indicator could partially explain why Ether could not withstand the adversity brought by Bitcoin's (BTC) 13% weekly negative move.

However, the leading altcoin has catalysts of its own because Ethereum developers implemented the network's first-ever "shadow fork" on April 11. The testnet update created an area for developers to stress-test their assumptions around the network's complex shift to proof-of-stake.

More importantly, one needs to analyze how professional traders are positioning themselves and there's no better gauge than derivatives markets.

The futures premium is back to bearish levels

To understand whether the current bearish trend reflects top traders' sentiment, one should analyze Ether's futures contracts premium, also known as a "basis." Unlike a perpetual contract, these fixed-calendar futures do not have a funding rate, so their price will differ vastly from regular spot exchanges.

A trader can gauge the market sentiment by measuring the expense gap between futures and the regular spot market. A neutral market should present a 5% to 12% annualized premium (basis) as sellers request more money to withhold settlement longer.

The above chart shows that Ether's futures premium stood above the 5% neutral threshold between March 25 and April 6, but later weakened to 3%. This level is typically associated with fear or pessimism because futures market traders are reluctant to open leveraged long (buy) positions.

Long-to-short data confirms worsening conditions

The top traders' long-to-short net ratio excludes externalities that might have impacted the longer-term futures instruments. By analyzing these whale positions on the spot, perpetual and futures contracts, one can better understand whether professionals effectively become bearish.

Firstly, one should note the methodological discrepancies between different exchanges, so the absolute figures have lesser importance. Yet, since April 5, there has been a considerable decline in the long-to-short ratio of every major derivatives exchange.

Data signals that whales have been increasing their bearish bets over the past week. For instance, the Binance whales held a 1.05 long-to-short ratio on April 5, but gradually reduced it to 0.88. Furthermore, the OKX top traders moved from a 2.11 favoring longs to the current 1.35.

( Marcel Pechman, Cointelegraph, 2022 )